Building a safety net means creating an emergency fund.

This is a stash of money set aside specifically to cover unexpected expenses.

You can’t think of it as an investment or a savings goal for a vacation, but rather it’s a financial buffer that keeps you from going into debt.

This post breaks down exactly how to start your emergency fund, even if your budget is tight.

You’ll learn how much you need, where to keep your money, and how to save smarter based on your income level.

Looking for Trustworthy Crypto Tips and Tools?

Visit Material Bitcoin for expert insights, secure cold wallets, and the latest news on crypto investing and self-custody.

What Is an Emergency Fund and Why You Need One in 2025

There are many major life events that require having some sort of emergency fund set aside.

💼❌Job loss

🏥💸Medical bills

🔧🏠💥Car/home repairs

How Much Do You Actually Need: 3, 6, or 12 Months?

Deciding on the ideal emergency fund isn’t an exact science.

It depends on your situation, although most financial experts agree that a minimum of 6 months should be the benchmark standard.

| Your Profile | Recommended Emergency Fund |

|---|---|

| Single, renting | Aim for 3 months of living expenses (rent, utilities, groceries) |

| Family with a mortgage | 6 months is safer, covering childcare, insurance, and housing |

| Self-employed or high-risk jobs | Consider 12 months to buffer against income fluctuations |

Did You Know❓

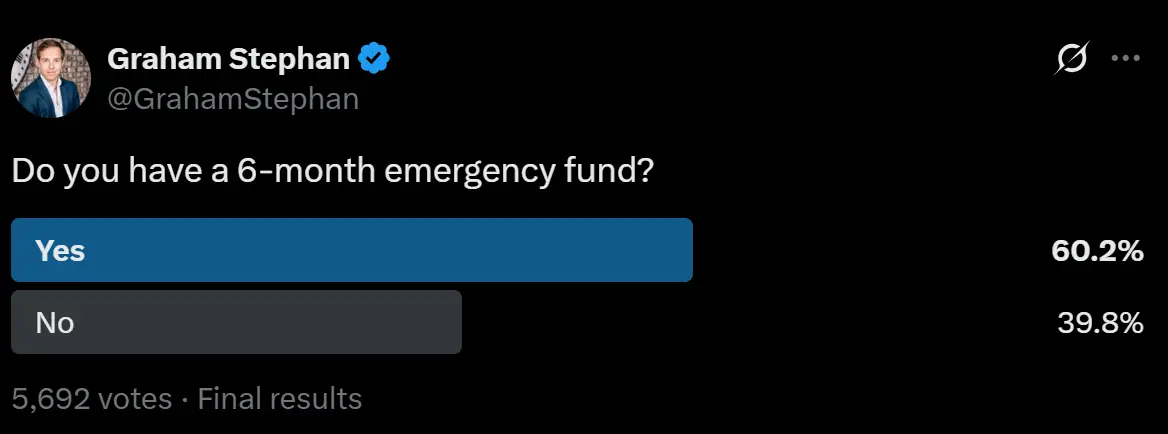

According to Bankrate’s January 2024 Emergency Savings Survey, 56% of Americans couldn’t afford a $1,000 emergency expense from their savings. 😬

Step-by-Step Guide to Start Your Emergency Fund from Zero

One of the first steps is to open a dedicated emergency savings account.

You might think, why do I need a new and separate account? Can’t I just know the amount I have set aside?

No.

Keeping your emergency fund distinct helps avoid “accidental” spending and tracks your progress clearly.

Account Types: HYSA vs. Traditional Savings

A High-Yield Savings Account (HYSA) is a type of savings account that earns significantly more interest than a regular one, often around 4–5% in 2025. It’s great for safely growing your emergency fund or short-term savings while keeping your money easily accessible.

| Account Type | APY (U.S.) | Pros | Cons |

|---|---|---|---|

| HYSA | Around 3%–4.5% | Higher interest, FDIC insured, pure savings | May have transfer limits |

| Traditional Savings | Around 0.01% | Broad access, easy to open | Almost no interest |

Top Platforms In the U.S. and Internationally

- Ally: No monthly fees, strong APY

- Wise: Multi-currency accounts

- Revolut: Global pockets, sub-savings and crypto features

Start Small and Scale Up

Once you’ve set up your account, you need to create a realistic goal.

💰Begin with a modest goal of $100 to build momentum.

📱Use visual trackers to help. Printable “savings thermometers” or mobile apps can help you visualize your progress and stay motivated.

🗓️Try a 52-week savings challenge: save $1 in week 1, $2 in week 2, … $52 in week 52. This will get you a total of $1,378 by the end of the year!

Where to Make Cuts Without Sacrificing Your Lifestyle

🔍 Audit your subscriptions

Pause or cancel unused services like Netflix, Spotify, or fitness apps you rarely use.

☕ Cut back on daily coffee runs

Brew at home instead of buying coffee out. Saving $3 per day adds up to over $1,000 per year.

🍽️ Limit food delivery and dining out

Swap one or two takeout meals per week for home-cooked alternatives.

🚗 Review transport expenses

Use public transit, bike, or carpool when possible.

🛍️ Know where your money goes

Use apps to track spending categories.

@mooremoneyclips Simple Ways to SAVE MONEY #money #economy #entrepreneur #tax #business #inflation #insurance #interest #savings #richvspoor #bank #banking #uktiktok ♬ original sound – mooremoneyclips

Using Stablecoins for Emergency Funds

Because crypto is viewed as a highly volatile asset, many stay away from it as a means of saving for an emergency fund.

But can stablecoins be a helpful backup?

| ✅ Pros | ⚠️ Cons |

|---|---|

|

|

For a beginner, using a HYSA is safest.

But adding a small, regulated stablecoin reserve (5–10% of the fund) can give you flexibility.

MATERIAL USDT

Tether ERC-20/EVM

$89

How to Build Your Emergency Fund Based on Your Income Level

Whether you are earning a smaller amount or a lot, there are always smart savings and investing strategies to fit your situation.

Saving on a Lower Income

Saving money when you’re earning a small income can feel impossible.

The key is to start small and be consistent.

- Use micro-savings apps to guide you. Apps like Acorns round up any purchase to save the spare change, while the Chime app can automatically set aside a percentage of your paycheck.

- Finding ways to make extra income can give your savings a boost. Try freelancing or doing odd jobs.

- Set small, realistic goals. Saving just $5 a day might not seem like much, but it adds up quickly in your emergency fund.

The goal isn’t to save millions right away, but rather to make progress.

Even if you can only save a little, building the habit to save and not spend puts you in a stronger position for the future.

Middle Income Range

When you’re making a decent amount, there are always ways to rearrange your finances to save more.

- Look for monthly bills to reduce (phone bills, subscriptions…)

- Use cashback tools. Many banks and platforms offer small rebates on groceries, gas, or dining.

- Try crypto cashback cards to turn your everyday spending into crypto rewards.

High Income

Most people assume that earning a large income means you can afford any crisis that comes along.

But in reality, there are always some surprises that might catch you off guard.

- Use “occasional” income like your tax refunds, bonuses, or crypto investment profits to add to your emergency fund.

- Build a diversified portfolio to earn more to later save.

- 40% to your emergency fund

- 30% to pay off debt

- 30% to invest

Mistakes to Avoid When Starting Your Emergency Fund

Starting an emergency fund is a smart move, but certain mistakes can slow you down.

Here are some of the most common mistakes and how to avoid them:

1️⃣ Keeping It in Cash or a Checking Account

You might think it’s safe to keep your emergency money in cash or your regular bank account, but both come with downsides:

| Storage Method | Pros | Cons |

|---|---|---|

| Cash | Immediate access | No interest, risk of loss or theft |

| Checking | Easy to use and track | No growth, too easy to spend accidentally |

| HYSA | Around 4.5% APY, FDIC insured, secure | May take 1–2 days to transfer funds to checking |

Tip: A HYSA is usually the best place for emergency funds. It’s safe, earns interest, and keeps your money separate from daily spending.

🏦 If you are wary of traditional banking, storing part of your emergency fund in stablecoins offers a decentralized alternative to your money.

This provides 24/7 access, global mobility, and freedom from bank restrictions, especially valuable in countries with limited financial infrastructure.

2️⃣ Mixing Your Emergency Savings with Daily Spending Money

One of the biggest mistakes is keeping your emergency savings in the same account as your everyday funds.

Without realizing it, you might dip into it, especially “just this one time.”

- Open a separate savings account at a different bank if you need to.

- Disable online transfers.

- Use nicknames like “Do Not Touch” to mentally reinforce boundaries.

3️⃣Setting Unrealistic Goals

Going too hard too fast can backfire.

Saving $1,000 a month sounds great and maybe easy to achieve, but it’s hard to maintain if you’re on a tight budget.

- Start small: try $100 a week or a % of each paycheck.

- Build the habit of saving, not spending.

View this post on Instagram

Tools and Apps That Make Emergency Saving Easier

Round-Up & Auto-Save Tools

- Use Qapital, Acorns, or Monzo to round up purchases and save the change

- Set daily auto-saves

- Try savings challenges: No-Spend November or 30-Day $5 Daily Save

Budgeting Apps That Prioritize Emergency Funds

- YNAB (You Need a Budget): assign every dollar a job, starting with your emergency fund

- Emma: tracks spending and helps prioritize savings goals

Tip: You don’t need to spend money on fancy apps. Using a good old Excel sheet to block out your fixed expenses and track your daily spending is a great place to start!

How to Know When Your Emergency Fund Is “Ready”

A healthy emergency fund takes time to grow.

Depending on your income level and fixed expenses, outlining a specific goal for your financial stability is what will keep you on track and reach a realistic objective.

Once your emergency fund is built, it’s time to shift your focus to building your wealth.

You can start investing in crypto with secure cold wallets like Material Bitcoin, set up long-term investments, or work towards enjoying a holiday.

Just remember: your emergency fund should always be available for any unforeseen problem.

FAQs

How much should I save in my emergency fund?

- Most experts recommend 3–6 months of essential expenses.

Where should I keep my emergency fund?

- A high-yield savings account (HYSA) is ideal; it’s safe, earns interest, and keeps your funds separate from everyday spending.

Can I use crypto for my emergency fund?

- Yes, stablecoins like USDC can offer flexibility and access without banks, but they carry regulatory and liquidity risks.

How do I start saving with a low income?

- Start small with $1–$5 per day using micro-savings apps or side gigs. Consistency matters more than the amount.

0 Comments