Financial planning is about creating a stable future.

Traditional finance is no longer the only way to build wealth, but instead has evolved to include new asset classes, like cryptocurrency.

As Bitcoin, Ethereum, and other stablecoins rise, knowing how to manage your finances is vital.

Crypto offers incredible benefits for a diverse investing portfolio, but it also introduces some unique risks.

Without having a solid financial plan and knowledge, you can fall victim to common financial planning mistakes.

Your Go-To Resource for Crypto Security & News

Stay informed with Material Bitcoin, your trusted source for crypto news, financial education, and self-custody tools. Whether you’re new to Bitcoin or building long-term wealth, we help you invest smarter and stay protected.

Top 10 Common Financial Planning Mistakes

From overspending and lack of budgeting to poor diversification and tax oversights, here are the most common financial planning mistakes you might be making and how to correct them.

1️⃣ Overspending

When your income rises, it’s normal to want to upgrade your lifestyle.

But if you lack a strong financial foundation, this behavior can lead to major problems.

Lifestyle Inflation

When your salary increases, you spend on short-lived luxury or trendy purchases.

This doesn’t have to be a Rolex watch or fancy trip; it can be a flashy NFT or super volatile memecoin.

During the 2021 crypto bull run, tokens like Dogecoin and Shiba Inu had massive (but temporary) gains.

Investors who bought SHIB in 2021 near its peak lost over 80% of their value within a year.

Who bought SHIB back in 2021 and still holding?…even if your still upside down?

byu/Spirited_Weakness211 inshib

Alternatively, building an emergency fund or buying Bitcoin during a dip would’ve been a much smarter financial move.

Bitcoin (BTC) closed at $105,472.41 (15-06-2025), reflecting a +263.8% increase since 2021. The most recent price stands at $106,945.86.

Lifestyle vs. Reinvestment

As income grows, you have two choices: spend more or reinvest.

A helpful strategy is to limit lifestyle upgrades to no more than 20% of any increase in income.

The remaining 80% can be redirected to savings, emergency funds, or long-term investments like Crypto index funds or BTC.

This helps to compound your wealth over time.

To protect your long-term crypto investments, use secure storage solutions like Material Bitcoin.

Our tamper‑proof physical cold wallet keeps your digital assets fully protected, air‑gapped, offline, and under your control.

2️⃣Skipping a Budget and Financial Plan

Budgeting is financial planning 101.

Without a clear plan, it’s easy to overspend, invest too much, or neglect debt.

Crypto Investors Also Need a Budget

A good budget helps you to stay in control during bear and bull markets, avoid emotional decision making, and build a consistent plan for long-term growth.

Try breaking down your budget as follows:

🟢 Fixed Costs (Rent, Bills, Groceries): 50%

🟡 Crypto Investing: 15%

🔵 Emergency Fund Savings: 10%

🟠 Fun / Entertainment Spending: 15%

🔴 Debt Payments: 10%

This split helps you balance everyday needs with long-term crypto goals, without going overboard.

3️⃣Not Having an Emergency Fund

An emergency fund is your safety net.

Without it, you might be forced to go into debt or even sell your crypto and other investments.

Many experts recommend saving a minimum of 3 to 6 months’ worth of essential expenses in a liquid, low-risk account.

This protects your investments and gives you peace of mind during unexpected events.

Where to Keep It? Fiat vs. Crypto

There are a few smart places to keep your emergency fund.

| Option | Pros | Cons |

|---|---|---|

| Bank Account | Safe, FDIC-insured, instantly accessible | Low or no interest |

| High-Yield Savings | Better interest, also secure | It may take 1–2 days to transfer |

| Stablecoins (Tether) | Can earn interest, ideal for crypto-native savers | Risk of depegging, not insured like banks |

4️⃣ Misusing Credit, Leverage, and Debt

In the US, many think that credit is no big deal.

Some even look at it as “free money“.

This couldn’t be further from the truth!

Don’t Confuse Credit with Capital

Using credit to invest in crypto is a super risky move.

Suppose you charge $3,000 to a credit card at 20% APR to buy Ethereum during a bull run.

If the price drops 40%, you lose $1,200 on your investment, and you still owe the full $3,000 plus interest.

This isn’t to say that ETH won’t bounce back in the long term, but if you are counting on a quick return to pay back your debt, you might be out of luck and in big trouble if your prediction is incorrect.

Debt Payoff

If you’re sitting on gains, consider using a small portion to eliminate high-interest debt.

For example, using a part of your altcoin profits to pay off a 20% credit card could “return” more than holding onto that asset in a down market.

5️⃣ Ignoring Retirement and Long-Term Wealth Planning

Some rely on their weekly paychecks to get by, while others are adding to their 401k.

But did you know that there is more you can do?

Fiat and Crypto Working Together

The earlier you start investing, the more you benefit from compound growth.

Even small investments grow significantly over time when reinvested regularly.

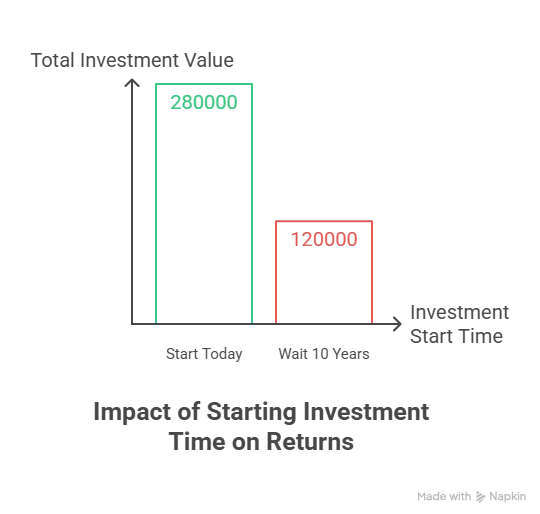

For example, if today you started to invest $200 monthly with an 8% annual return, over 30 years, you would have over $280,000.

Versus, if you wait 10 years to begin, that total would drop to $120,000.

This works for both fiat and crypto investments.

The key is to start and not wait to save up a large sum to buy.

6️⃣ Lack of Diversification and Emotional Investing

We’ve all heard the expression “don’t put your eggs in one basket”, but you also don’t want to buy any coin that comes out on the market.

You need to do your research and be selective.

Don’t Go All-In on One Coin

Diversifying across different sectors and assets can help reduce risk.

A simple diversified crypto portfolio might include:

| Asset Type | Example | Allocation (%) |

|---|---|---|

| Bitcoin (Store of Value) | BTC | 40% |

| Ethereum (Smart Contracts) | ETH | 30% |

| DeFi Tokens | AAVE, UNI, COMP | 10% |

| Stablecoins | USDC, USDT | 10% |

| Other (Layer 1s, NFTs, etc.) | SOL, AVAX, MATIC | 10% |

If you’re a beginner in crypto, starting to invest only in Bitcoin and Ethereum might be a better choice.

These coins historically function well and give you the ability to test out and get used to the crypto market before jumping into the more complex world of NFTs, DeFi, and other crypto projects.

Panic Selling

Crypto markets are known for being volatile, but history shows that they usually rebound.

Panic selling during a dip will often cause greater losses that could’ve been avoided with patience and planning.

View this post on Instagram

7️⃣ Not Rebalancing or Reviewing Your Plan

Your financial plan should evolve with your life.

Not reviewing it is one of the most overlooked common financial planning mistakes.

Review it quarterly and after major changes in your life, like a new job, a market crash, marriage, birth of a child, or a big purchase.

Rebalancing Portfolio

Regular rebalancing keeps your risk in check.

8️⃣ Underestimating Insurance and Estate Planning

If you have dependents or large assets, considering insurance is a useful option.

A life insurance policy helps to ensure that your family won’t have financial stress if something happens to you.

This can even include paying capital gains taxes or inheritance taxes once you pass.

If you’ve built a strong crypto portfolio, you need a plan to protect and pass it on.

Estate Planning: Protecting Digital Assets

Crypto is unique since there are no banks or regulated recovery systems in place if something happens to you.

Without clear instructions and access, your crypto assets could be lost forever.

✅ Simple Estate Planning Checklist for Crypto

| 📝 | Create a will that includes your crypto holdings. |

| 🔐 | Use a password manager to store wallet credentials securely. |

| 👤 | Name a trusted person as a beneficiary or backup holder. |

| 📦 | Keep seed phrases and recovery instructions in a secure place. |

9️⃣ Overlooking Tax and Hidden Costs

Many people don’t realize that every trade is a taxable event, even swapping one token for another.

In the US, the IRS and other tax authorities treat crypto as property, meaning capital gains taxes apply whenever you sell or trade an asset.

‼️Example: If you swap ETH for SOL, that counts as a sale of ETH. If it gained value since you bought it, you owe tax on the profit.

📊 Short-Term vs. Long-Term Capital Gains (U.S.)

| Holding Period | Tax Type | Approx. Rate |

|---|---|---|

| Less than 1 year | Short-term capital gains | Taxed as ordinary income (10–37%) |

| More than 1 year | Long-term capital gains | 0%, 15%, or 20%, depending on income |

Tip: Check out our global crypto tax guide for more on how to stay compliant while keeping your assets safe in cold storage.

🔟 Ignoring Your Emotions and Behavior

Emotions can ruin even the best investing strategies and plans.

Feelings of FOMO, panic selling, and loss aversion will lead you to poor timing and impulsive decisions, especially when crypto is falling quickly.

You can use simple tricks like dollar-cost averaging, stick to a long-term plan, and only invest what you can afford to lose.

Storing your crypto safely in a non-custodial wallet like Material Bitcoin will also reduce the urge to react emotionally, keeping your focus on long-term goals.

Build Smarter Habits for Long-Term Success

Financial planning is just as important in crypto as it is in any other form of investing.

Avoiding common financial planning mistakes like overspending, skipping budgeting, tax obligations, or investing emotionally, can make the difference between your success and downfall.

Start small, stay consistent, and protect your crypto with Material Bitcoin.

0 Comments